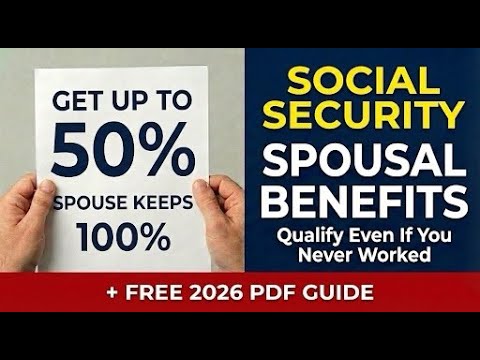

Social Security Survivor Benefits 2026: The Strategy Most Widows Miss

If you’ve recently lost a spouse, parent, or ex-spouse, Social Security survivor benefits could provide you with monthly income for the rest of your life — but only if you know how to claim them correctly. About 5.8 million Americans currently receive Social Security survivor benefits, including roughly 3.5 million widows and widowers and 2.1 million children of deceased workers. Many more qualify but never apply.

This 2026 guide walks you through who qualifies, how much you’ll receive, the strategic claiming decision most widows miss, and the six costliest mistakes to avoid.

Who Qualifies for Social Security Survivor Benefits in 2026

Several groups can qualify on a deceased worker’s earnings record:

- Surviving spouses can claim as early as age 60 (or age 50 if disabled, or any age if caring for the deceased’s child under 16)

- Divorced spouses qualify if the marriage lasted at least 10 years and they are currently unmarried (or remarried after age 60)

- Unmarried children under 18, or up to 19 if a full-time high school student, or any age if disabled before age 22

- Dependent parents age 62 or older who relied on the deceased for at least half their financial support

If you were divorced from the deceased and your marriage lasted 10+ years, you may be entitled to benefits on their record — and your claim does not reduce anyone else’s. This is one of the most overlooked categories in the entire Social Security system.

How Much You’ll Receive

Survivor benefits are based on the deceased worker’s Primary Insurance Amount (PIA):

- Surviving spouse at full retirement age: 100% of the deceased’s benefit

- Surviving spouse, age 60 to FRA: 71.5% – 99% (depending on age)

- Surviving spouse caring for child under 16: 75% (no minimum age for you)

- Each eligible child: 75% of the deceased’s basic benefit

There’s also a family maximum that caps total benefits to one family at roughly 150%–180% of the worker’s basic benefit.

Keep in mind: if the deceased claimed their own retirement benefit early (before their full retirement age), a special rule called the Retirement Insurance Benefit Limitation (RIB-LIM) applies. Even if you wait until your full retirement age to claim, your survivor benefit is capped at the higher of the deceased’s reduced amount or 82.5% of their PIA.

The Switch Strategy — The Decision Most Widows Miss

If you have your own Social Security work record, you do not have to claim your retirement and your survivor benefit at the same time. You can claim one early at a reduced rate, then switch to the other later when it’s worth more.

- Path A: Claim survivor benefits as early as age 60 → let your own retirement keep growing → switch to your own retirement at age 70 when it’s at its maximum

- Path B: Claim your own reduced retirement benefit early → switch to the full survivor benefit at your full retirement age

Done correctly, this single decision can mean tens of thousands of dollars more over your lifetime. Run the numbers — or have an SSA representative run them — before you commit. If you also need to understand how this interacts with your own retirement planning, our guide on SSDI vs. Social Security Retirement covers the related decision points.

How to Apply (You Cannot Apply Online)

Here’s the first surprise: you cannot apply for survivor benefits online. This is one of the few Social Security benefits that requires a phone call or in-person visit.

- Call SSA at 1-800-772-1213 (Mon–Fri, 8:00 AM – 7:00 PM local time)

- Or visit your local Social Security office (find one at ssa.gov/locator)

Documents you’ll need: death certificate, your Social Security number and the deceased’s, your birth certificate, marriage certificate (or divorce decree), birth certificates for any dependent children, the deceased’s most recent W-2 or self-employment tax return, and bank account info for direct deposit.

The funeral home usually reports the death to Social Security — but don’t assume. Confirm it happened and follow up directly. Apply as soon as possible — retroactivity is limited.

2026 Earnings Test Limits

If you’re working while receiving survivor benefits, the retirement earnings test can reduce your check:

- Under full retirement age all year: Earn up to $24,480 before SSA withholds any benefits

- Reaching full retirement age in 2026: Limit jumps to $65,160 for the months before your birthday

- At or after full retirement age: No limit at all

Withheld benefits aren’t lost — once you reach FRA, SSA recalculates upward to account for any months that were withheld.

6 Costly Mistakes to Avoid

- Not knowing you qualify. Divorced spouses miss out the most.

- Claiming too early. The reduction is permanent for life.

- Skipping the switch strategy. Most people claim one benefit and never look back.

- Assuming the online portal works. It doesn’t.

- Missing the $255 lump-sum death benefit. Two-year deadline, easy to forget.

- Remarrying before age 60. That disqualifies you from survivor benefits on your late spouse’s record. Wait until 60 and you keep them.

2025 Social Security Fairness Act — Major Update for Public-Sector Workers

The Social Security Fairness Act, signed January 5, 2025, fully repealed both the Government Pension Offset (GPO) and the Windfall Elimination Provision (WEP) — retroactive to January 2024.

If you’re a teacher, firefighter, police officer, or other public-sector worker whose survivor benefit was previously reduced or denied because of GPO, you now qualify for the full benefit. SSA completed the bulk of automatic retroactive payments by July 2025, but if you never applied because of the old rules, apply now — you may be entitled to back benefits all the way to January 2024.

For more on understanding your own work history, see our guide on How to Check Your Social Security Earnings Record.

Free Step-by-Step PDF Guide

We’ve put together a complete free PDF guide on everything covered in this video — eligibility for every category, the switch strategy worked out with examples, the full document checklist, the 2026 earnings test, the SSFA back-pay process, and the $255 lump-sum benefit families forget to claim.

Browse all our guides on the Free Government Guides page.

Subscribe to GovClarity on YouTube for new step-by-step guides every week.

Frequently Asked Questions

Surviving spouses can claim from age 60 (or 50 if disabled), divorced spouses if married 10+ years and currently unmarried, unmarried children under 18 (or 19 if in high school, or any age if disabled before 22), and dependent parents 62 or older.

Surviving spouses at full retirement age receive 100% of the deceased’s benefit. Between age 60 and FRA, you receive 71.5% to 99% based on age. Spouses caring for a child under 16 get 75% with no minimum age. Each eligible child receives 75%.

Yes. Divorced spouses qualify if the marriage lasted at least 10 years and they are currently unmarried, or remarried after age 60. Your claim does not reduce anyone else’s benefit. This is one of the most overlooked categories in the entire Social Security system.

If you have your own work record, you can claim survivor benefits early at a reduced rate, then switch to your own retirement benefit at age 70 when it’s at maximum. Or claim your own reduced retirement first and switch to full survivor benefits at FRA.

No. Survivor benefits are one of the few SSA benefits that cannot be applied for online. You must call 1-800-772-1213 (Mon-Fri 8 AM to 7 PM local time) or visit your local Social Security office. Apply as soon as possible — retroactivity is limited.

If you are under full retirement age all year, you can earn up to $24,480 before SSA withholds benefits. If you reach FRA in 2026, the limit jumps to $65,160 for months before your birthday. After FRA there is no earnings limit at all.

SSA pays a one-time $255 lump-sum death benefit to a surviving spouse or dependent child of a deceased worker. The deadline to apply is two years from the date of death. Call 1-800-772-1213 to request it — it is easy to forget.

Signed January 5, 2025, the Act fully repealed the Government Pension Offset (GPO) and Windfall Elimination Provision (WEP) — retroactive to January 2024. Public-sector workers previously denied or reduced survivor benefits now qualify for the full amount, with possible back benefits.