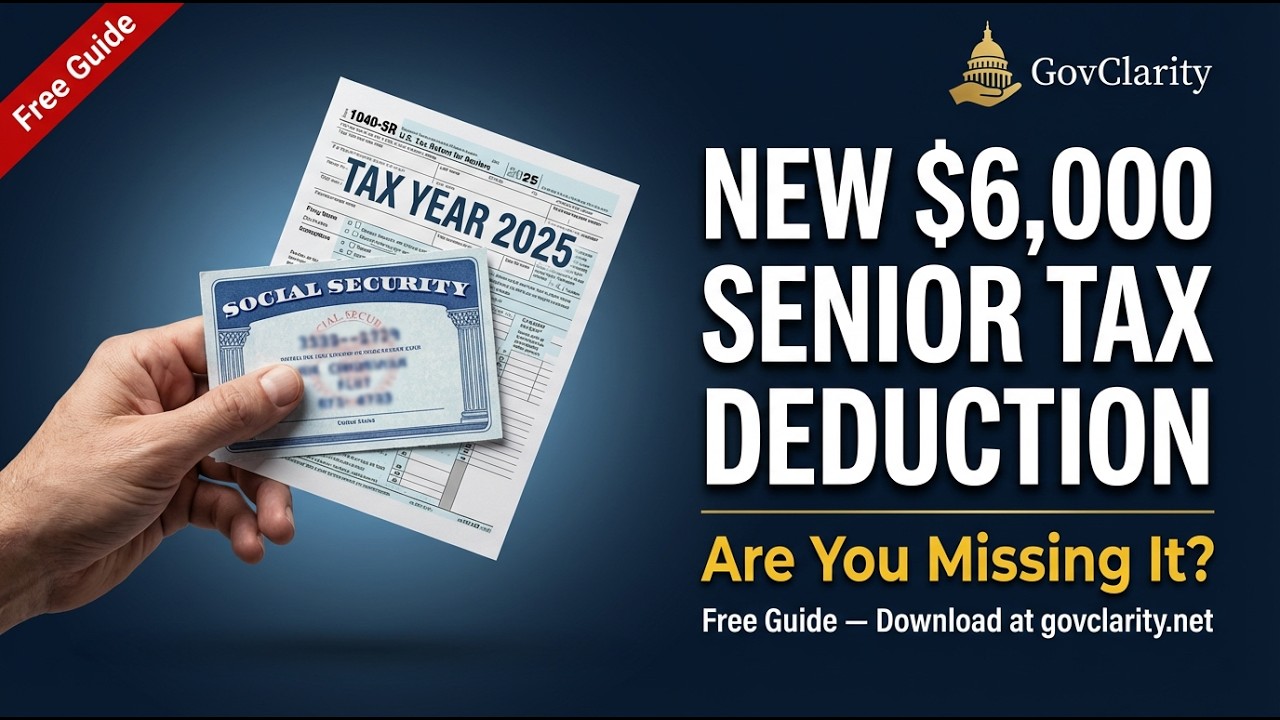

Senior Tax Deduction: How to Claim the New $6,000 Deduction for Seniors

If you’re sixty-five or older, the new Enhanced Deduction for Seniors could reduce your federal income tax by up to $6,000 per person — or $12,000 for married couples where both spouses qualify. This deduction was created by the One Big Beautiful Bill Act, signed into law on July 4, 2025, and it’s available right now for the 2025 tax year.

But here’s what makes this deduction unusual — it stacks on top of every other senior tax break you already receive. That means a single senior taking the standard deduction can now shield up to $23,750 from federal income tax. For a qualifying married couple, that number jumps to $46,700. In this guide, we break down exactly who qualifies, how to calculate your deduction, and how to claim it on the new Schedule 1-A.

Who Qualifies for the Senior Tax Deduction?

Three things must be true to claim this deduction:

- You must have been born on or before January 1, 1961. The IRS considers you sixty-five on the day before your birthday, so anyone born on January 1, 1961 qualifies for the 2025 tax year.

- You must have a valid Social Security number. ITIN holders do not qualify. If you’re married filing jointly and both spouses want to claim the deduction, both must have valid SSNs.

- You must file as Single, Head of Household, Married Filing Jointly, or Qualifying Surviving Spouse. Married Filing Separately results in a $0 deduction.

The deduction works whether you take the standard deduction or itemize. You do not have to choose between them.

How the Three Deductions Stack

The most common mistake seniors are making is confusing the new enhanced deduction with the existing additional standard deduction. They are two completely separate benefits, and you can claim both.

Component 1 — Base Standard Deduction: $15,750 (single) / $31,500 (joint)

Component 2 — Additional Standard Deduction for Age 65+: $2,000 (single) / $1,600 per spouse (joint). This has existed for years.

Component 3 — Enhanced Senior Deduction (NEW): $6,000 per qualifying person / $12,000 (joint, both qualifying). This is the new benefit from the One Big Beautiful Bill Act.

Total for a single senior: $23,750. Total for a qualifying married couple (both 65+): $46,700.

Income Phase-Out: Who Gets the Full Deduction?

- Single / Head of Household: Full deduction below $75,000 MAGI. Phases out completely at $175,000.

- Married Filing Jointly: Full deduction below $150,000 MAGI. Phases out completely at $250,000.

The reduction is 6% of every dollar above the threshold — or $60 for every $1,000 over the limit. Remember that all income sources count toward MAGI — taxable Social Security benefits, pension distributions, required minimum distributions, investment income, and part-time wages.

How to Claim It: Schedule 1-A, Part V

- Calculate your MAGI in Part I (usually your AGI from Form 1040, Line 11b)

- Complete Part V — enter the number of qualifying persons (1 or 2)

- Enter the base deduction ($6,000 or $12,000)

- Apply the phase-out reduction if your MAGI exceeds $75,000 (single) or $150,000 (joint)

- Your final deduction transfers to Form 1040, Line 13b

Below the Line: What This Deduction Does NOT Do

The Enhanced Senior Deduction is a “below-the-line” deduction. It reduces your taxable income but does not reduce your Adjusted Gross Income (AGI). This means it won’t help with Medicare IRMAA surcharges, Social Security benefit taxation thresholds, or premium tax credits — those are all based on AGI.

State Tax Warning

Not all states have adopted this deduction. States like California and Arizona haven’t conformed to the One Big Beautiful Bill Act, which means you may owe state income tax on income that’s exempt at the federal level. Check your state’s conformity status before counting on a state-level benefit.

Common Mistakes to Avoid

- Confusing the enhanced deduction with the additional standard deduction — these are two separate benefits that stack.

- Thinking you need to itemize — the deduction works with either the standard deduction or itemized deductions.

- Filing Married Filing Separately — MFS results in a $0 deduction.

- Missing the age cutoff — you must have turned sixty-five by December 31, 2025.

- Underestimating your MAGI — Social Security, pensions, RMDs, and investment income all count.

- Assuming your state honors the deduction — check your state’s conformity status first.

Key Details at a Glance

- Maximum deduction: $6,000 (single) / $12,000 (joint, both qualifying)

- Tax years covered: 2025 through 2028

- Phase-out begins: $75,000 MAGI (single) / $150,000 (joint)

- Phase-out ends: $175,000 (single) / $250,000 (joint)

- Form required: Schedule 1-A, Part V (Form 1040 or 1040-SR)

- Who qualifies: Taxpayers born on or before January 1, 1961, with a valid SSN

Download the Free Guide

Our free companion guide includes the complete stacking math, a printable phase-out calculator worksheet, state tax conformity table, strategic planning tips, and a step-by-step Schedule 1-A walkthrough.

Frequently Asked Questions

Created by the One Big Beautiful Bill Act, the Enhanced Deduction for Seniors lets qualifying taxpayers 65 or older deduct $6,000 per person, or $12,000 for married couples where both spouses qualify. It works with both the standard deduction and itemized deductions.

You must have been born on or before January 1, 1961, have a valid Social Security number, and file as Single, Head of Household, Married Filing Jointly, or Qualifying Surviving Spouse. Married Filing Separately results in a $0 deduction with no exceptions.

The new $6,000 enhanced deduction stacks on top of the existing $2,000 additional standard deduction for age 65+ and the base standard deduction. A qualifying single senior can shield up to $23,750 from federal income tax. A qualifying married couple can shield $46,700.

Single and Head of Household get the full deduction below $75,000 MAGI, phasing out completely at $175,000. Married Filing Jointly gets the full amount below $150,000 MAGI, phasing out at $250,000. The reduction is 6% — or $60 per $1,000 over the limit.

No. The Enhanced Senior Deduction works whether you take the standard deduction or itemize — you do not have to choose between them. This is one of the most common misunderstandings about the new benefit. You claim it in addition to whichever main deduction you elect.

No. It is a below-the-line deduction that reduces taxable income but not Adjusted Gross Income. That means it will not help with Medicare IRMAA surcharges, Social Security benefit taxation thresholds, or premium tax credits — those are all calculated based on AGI.

Not all states have adopted the deduction. States like California and Arizona have not conformed to the One Big Beautiful Bill Act, so you may owe state income tax on income that is exempt at the federal level. Check your state’s conformity status before filing.

Use Schedule 1-A Part V attached to Form 1040 or 1040-SR. Calculate MAGI in Part I, enter the number of qualifying persons in Part V, enter the base deduction ($6,000 or $12,000), apply phase-out if needed, then transfer to Form 1040 Line 13b.