No Tax on Overtime: How to Save Thousands on Your 2026 Taxes

The new No Tax on Overtime rule could save hourly workers hundreds or even thousands of dollars on their 2026 tax return. Under the One Big Beautiful Bill Act, qualifying workers can now deduct the overtime premium — the extra pay above your base rate — from federal income tax. If you earned $15,000 in total overtime pay at time-and-a-half, that’s a $5,000 deduction.

But this isn’t a full exemption on all overtime pay — it’s a deduction on the premium portion only. Your overtime still gets reported as income. The deduction reduces how much of that income gets taxed. In this video, we break down exactly who qualifies, how to calculate your deduction, and how to claim it correctly on the new Schedule 1-A.

Who Qualifies for the Overtime Deduction?

Two things must be true to claim this deduction:

- You must be a non-exempt employee under the FLSA. The Fair Labor Standards Act classifies most hourly workers as non-exempt — warehouse workers, nurses, retail staff, construction workers, manufacturing employees, food service workers, and many others. If your employer is legally required to pay you overtime when you work more than 40 hours a week, you likely qualify.

- You must have a valid Social Security number. ITIN holders do not qualify. Your SSN must be issued before the due date of your return, including extensions.

Workers who do not qualify include salaried exempt employees (managers, executives, administrative professionals), independent contractors and self-employed workers (1099-NEC recipients), married couples filing separately (deduction is $0), and federal employees classified as FLSA-exempt.

Understanding the Overtime Premium

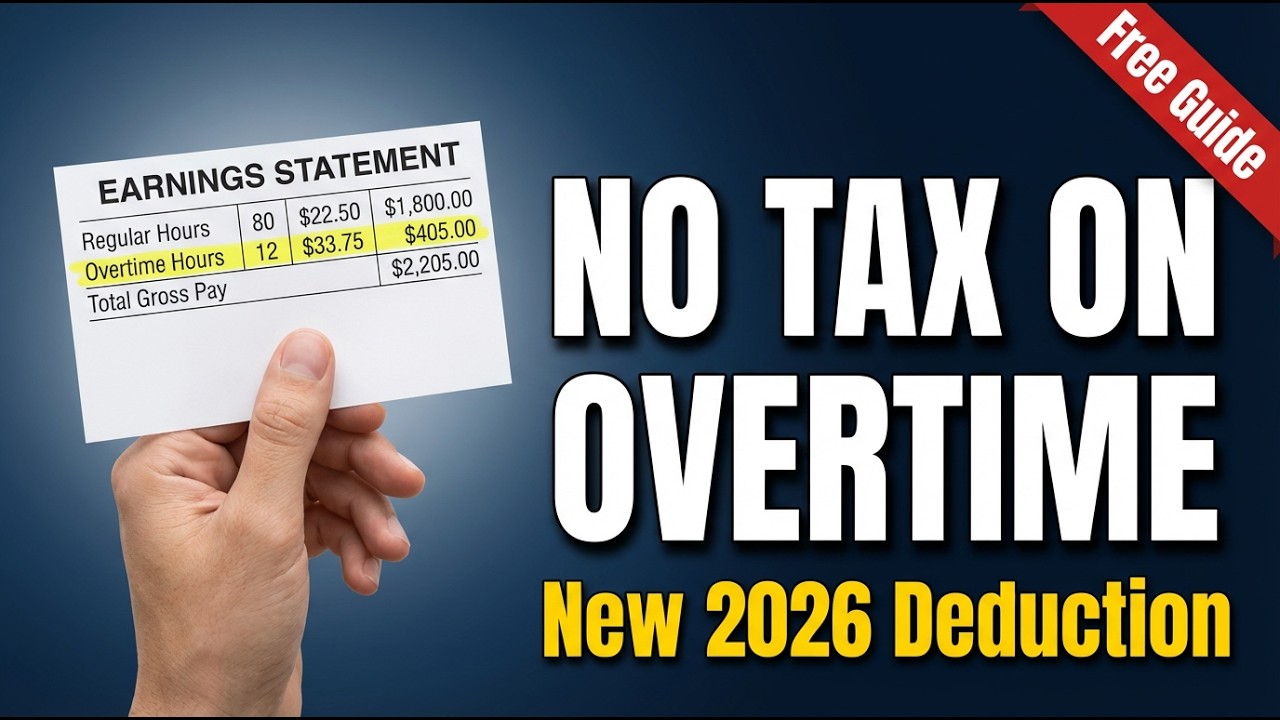

This is the part most people get wrong. The deduction does not cover your full overtime pay — only the premium, which is the extra amount above your base hourly rate.

If you earn $25 per hour and work overtime at time-and-a-half ($37.50/hour), only the $12.50 premium per hour is deductible — not the full $37.50. The IRS provides a simple shortcut formula: divide your total overtime pay by 3. So $15,000 in total overtime pay at 1.5x equals a $5,000 deduction.

For double-time workers, divide by 4. For mixed rates, you’ll need to calculate each rate separately.

Income Phase-Out: Who Gets the Full Deduction?

The deduction phases out at higher income levels based on your Modified Adjusted Gross Income (MAGI). Single and Head of Household filers get the full deduction up to $150,000 MAGI, phasing out completely at $275,000. Married Filing Jointly filers get the full deduction up to $300,000 MAGI, phasing out completely at $550,000.

The reduction is $100 for every $1,000 your MAGI exceeds the threshold. The maximum deduction is $12,500 (single) or $25,000 (married filing jointly).

How to Claim It: Schedule 1-A

You’ll claim this deduction using the new Schedule 1-A, attached to your Form 1040. Calculate your MAGI in Part I, enter your qualified overtime compensation (the premium amount) in Part III, enter the statutory cap ($12,500 single / $25,000 joint), enter the lesser of those two amounts, apply the phase-out reduction if your MAGI exceeds the threshold, and your final deduction transfers to Form 1040, Line 13b.

This deduction works alongside your standard or itemized deductions — not instead of them.

Common Mistakes to Avoid

- Deducting your full overtime pay instead of just the premium. Only the extra amount above base rate is deductible. Using total OT pay will trigger a CP2000 notice from the IRS.

- Forgetting that payroll taxes still apply. This deduction only covers federal income tax. Social Security and Medicare taxes (7.65%) still apply to every dollar of overtime.

- Claiming the deduction as an independent contractor. The FLSA only covers W-2 employees. If you receive a 1099-NEC, you are not eligible.

- Guessing your overtime amount. Without employer reporting this year, some filers enter a rounded estimate instead of calculating from actual pay records. Use the IRS formula and your pay stubs.

- Filing Married Filing Separately to double the deduction. It does not work — MFS filers get a $0 deduction by law.

If you also earn tip income, the tip income deduction may stack with your overtime savings — see how in our guide: No Tax on Tips 2026: How to Save Up to $25,000 on Your Taxes.

Key Details at a Glance

- Maximum deduction: $12,500 (single) / $25,000 (joint)

- Tax years covered: 2025 through 2028

- Phase-out begins: $150,000 (single) / $300,000 (joint)

- Form required: Schedule 1-A, Part III (Form 1040)

- Who qualifies: FLSA non-exempt employees with a valid SSN

Download the Free Guide

Our free companion guide includes the complete FLSA eligibility test, IRS calculation formulas with examples, a printable overtime calculator worksheet, income phase-out charts, a step-by-step Schedule 1-A walkthrough, and common mistakes to avoid.

This is Video 3 in our 2026 Tax Changes series. Watch Video 1: 7 New Tax Changes for the overview, Video 2: No Tax on Tips for the deep dive on tip income, and subscribe to GovClarity on YouTube for new guides every week.

Frequently Asked Questions

Created by the One Big Beautiful Bill Act, the deduction lets qualifying workers deduct the overtime premium — the extra pay above your base rate — from federal income tax. It is a deduction on the premium portion only, not a full exemption on all overtime pay.

You must be a non-exempt employee under the Fair Labor Standards Act and have a valid Social Security number. Salaried exempt workers, independent contractors, married couples filing separately, and federal employees classified as FLSA-exempt do not qualify.

For time-and-a-half overtime, divide total overtime pay by 3 — only the premium half is deductible. For double-time, divide by 4. So $15,000 in overtime at 1.5x equals a $5,000 deduction. The IRS provides this shortcut formula on Schedule 1-A.

The cap is $12,500 for single filers and $25,000 for married filing jointly. The deduction phases out at $150,000 MAGI (single) or $300,000 (joint), reducing $100 for every $1,000 above the threshold. It zeroes out at $275,000 single or $550,000 joint.

No. The deduction only covers federal income tax. Social Security and Medicare taxes (7.65%) still apply to every dollar of overtime pay. The deduction reduces taxable income but does not exempt wages from payroll taxes of any kind.

Single and Head of Household get the full deduction up to $150,000 MAGI, phasing out completely at $275,000. Married Filing Jointly gets the full amount up to $300,000 MAGI, phasing out at $550,000. The reduction is $100 for every $1,000 over.

No. The Fair Labor Standards Act only covers W-2 employees. If you receive a 1099-NEC for self-employment or contract work, you are not eligible for the No Tax on Overtime deduction regardless of how many hours you worked or how you are paid.

Use the new Schedule 1-A attached to Form 1040. Calculate MAGI in Part I, enter qualified overtime compensation (the premium amount) in Part III, apply the cap and phase-out, then transfer the final deduction to Form 1040 Line 13b. It works alongside standard or itemized deductions.